Is it possible to save money by combining maternity coverage with health insurance?

The coverage entirely depends on the type of plan and insurer that one selects and so the costs can vary.

Thousands of couples prepare to welcome the joys of parenthood each year. Many of them are prepared for the most important event of their lives, having purchased health insurance policies to cover all costs associated with childbirth. However, there may be unanticipated costs associated with pregnancy complications. Furthermore, any savings on hospitalization costs are dependent on the type of health policies that they have adopted.

The first step toward lowering hospitalization costs is to select the appropriate insurance policy. For example, a husband and wife who have separate health insurance policies with maternity insurance may be able to save more money because they can both make claims from their respective policies.

In indemnity-based policies, you can make claims from multiple policies up to the total amount of expenses or losses incurred, subject to the terms of the policies. As a result, if both parents have maternity coverage through their employer's policies, they should be able to make claims under both these policies.

Because the cost of healthcare is rising at an alarming rate, health insurance policies that include maternity coverage can help you save money on hospitalization. Expenses are extremely high these days due to rising inflation. These policies assist families in covering the costs of childbirth and the newborn's medical expenses.

However, as these policies come with a mandatory waiting period, it is important to carefully choose the maternity insurance so that the policyholders can benefit

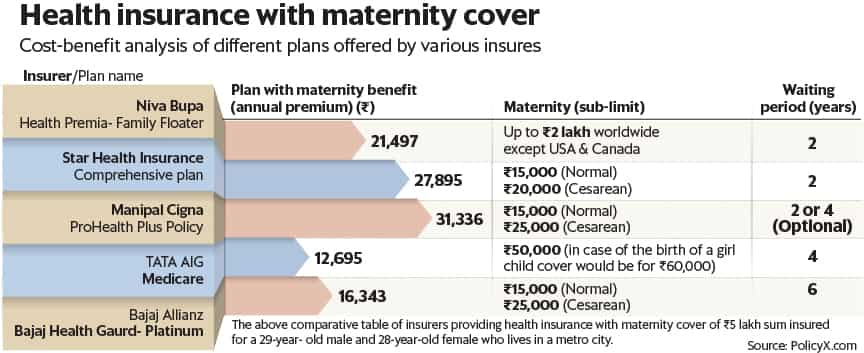

Waiting period: A period during which the insured is unable to claim any or all policy benefits from the insurer. This varies by insurer and policy, but the typical waiting period for such a policy with maternity cover ranges from 9 months to 4 years. Care Health Insurance, for example, has a policy called Joy Today with a nine-month waiting period. However, because it is a three-year policy, you must pay the premium for all three years in one go. As a result, before claiming any medical-related expenses, it is important to check your policy's waiting period.

Policy coverage: Health insurance with maternity coverage typically covers both normal and cesarean delivery. It can be purchased as a stand-alone policy or as an add-on to the base health policy (by paying some additional amount). A health insurance policy with maternity coverage typically covers hospitalization expenses during both the pre- and post-natal stages, newborn expenses (up to 90 days), daycare treatment, newborn vaccination expenses, ambulance expenses, cashless claim facilities, and so on. This coverage, however, is entirely dependent on the type of policy and insurer you choose, and thus may vary.

Pre-existing diseases that could possibly affect pregnancy, treatment expenses related to infertility, any medicinal expenses outside of the treatment purview, prenatal and postnatal expenses with no hospitalization, expenses involved in harvesting or storing stem cells, and so on are some of the common exclusions under this type of health coverage.

These policies are not available to women who are already pregnant. Furthermore, those who are not between the ages of 18 and 45 are not eligible to purchase such policies.

Sub-limits: The sub-limit clause states that your insurance will only cover a certain amount of the cost of certain procedures. In other words, a sub-limit is a monetary limit imposed by your insurer on a specific medical insurance claim. They are frequently represented as a fixed amount, but they can also be expressed as a percentage of the total sum insured. "Most insurers usually limit their maternity payouts. In general, normal delivery sub-limits range from 15,000 to 25,000, whereas cesarean delivery sub-limits range from 25,000 to 50,000. (depending on the type of policy and insurer)

Policy cost: The cost of such policies is determined by factors such as the type of insurance, the age of the policyholders, the area pin code, the sum insured, and so on. The premiums for such covers are typically on the higher end because the likelihood of a claim being filed is high under this cover. You must conduct thorough research and compare the options available online in order to find the best policy that meets both your needs and your budget.

So, when you decide to buy such coverage, you should undertake a detailed cost-benefit analysis between different policies offered by various insurance providers.